In the following couple of posts I have to come back to IOF finances. Over the past two months I talked to several members of the Council. I had to realize that either they did not understand the severity of the financial situation, or did not really appreciate it. “We have lot’s of cash in the bank” and “I am positive that everything will be fine” were the typical replies when we talked about IOF finances.

So let’s have a closer look at the net cash position of the IOF on 31 December 2016, the date of the last audited accounts, as published on the IOF website. Below I’ll try to explain the accounting basics required to interpret the numbers.

There are two key points people concerned about the IOF should understand:

The net cash position of the IOF is practically zero. In simple terms: there is substantial money on the bank account only because there are substantial unpaid invoices.

The IOF has started to accumulate serious debt. Short term debt has jumped almost ninefold from €29,000 to €252,000 in one year from end 2015 to end 2016.

Net cash position shows the real amount of cash reserves assuming that all current invoices are paid (including consumed services not yet invoiced), and all current outstanding receipts are paid (including revenues earned, but not yet invoiced). There are variations to this calculation, due to the sad fact of life that it is more likely that you have to pay for services consumed, than that everybody pays you all the money you expect from them. It is always a question how to find the right balance between the optimistic and the prudent approach. Here we make adjustments only when there is a clear indication that not all the monies may be received.

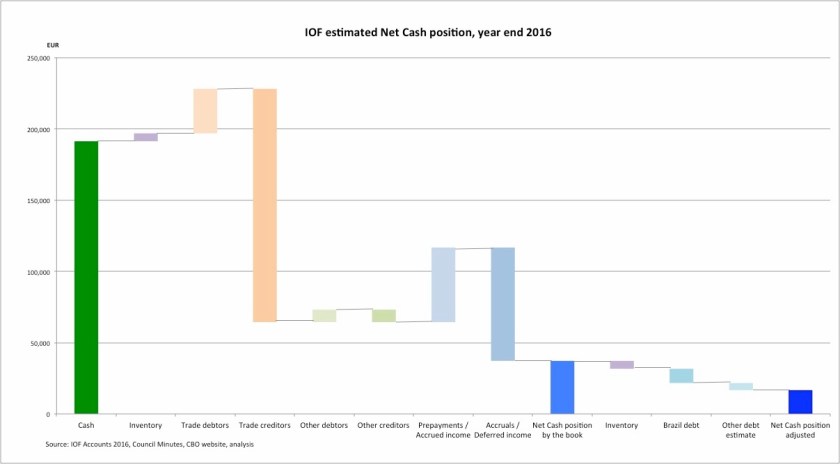

On the chart below you can see the estimated net cash position of the IOF at the end of year 2016. It shows the accounting book values and it is also adjusted for items that are unlikely to be “cash equivalent” (like inventory and Brazilian debt) and an estimated “membership debt” referred to in Council minutes.

Despite the €191,000 in the bank, the net cash position of the IOF was only €37,000. Taking into account adjustments, the actual net cash is estimated at around €16,000.

At €16,000 (or even at €37,000) the IOF has practically no meaningful net cash reserves for its annual budget of €800,000 to €900,000. The budget overrun in early 2017 only for the World Games arena production was at around €20,000!

It should be noted that the revised budget of 2017 will not solve the problem. The new forecast is a profit of just above zero: €10,000. It was reduced from €70,000 planned for 2017 in August 2016. That, even if delivered, will not change principally the difficult financial situation of the IOF.

Below I’ll explain the various items for a better understanding.

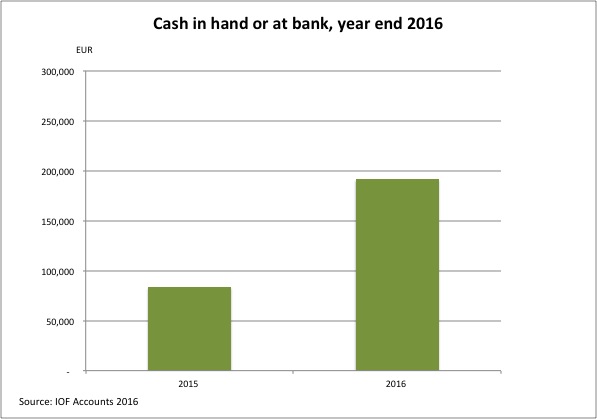

Cash

That is self explanatory. Cash in hand and at banks. The amount at €191,000 looks sufficiently large (over 20% of the budget). It is €110,000 more than in 2015.

Unfortunately, the reason is that the value of unpaid bills (trade creditors) from 2015 to 2016 increased by €160,000!

The IOF cash position looks good only because piles of invoices are waiting to be paid…

Inventory

This is a small, but unusual item at €5000. These could be brochures or similar items. Unlikely that they have a monetizable value. They are part of the accounting calculation, but for practical reasons it is likely to be a deductible item.

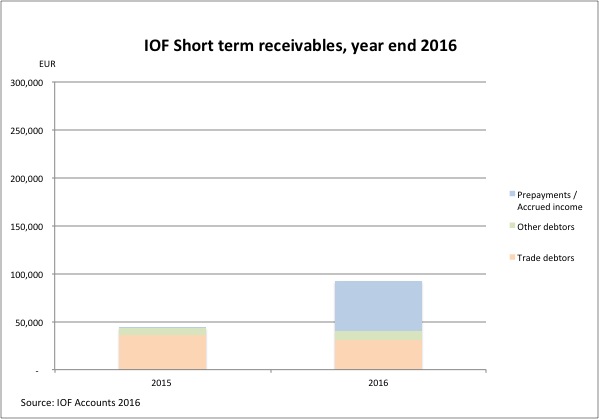

Trade debtors

These are monies that were not paid yet on invoices issued by the IOF. Similar value as last year, around €31,000. These include for example outstanding membership fees and outstanding sanction fees like the €10,000 remaining from the Brazilian debt from WMOC 2014.

Considering the total budget of €800,000 to €900,000, the IOF is blessed with a very reliable source of revenue with less than 4% or trade debtors. Apparently orienteers have a remarkable tax paying discipline. But if there is any delay in payments to the IOF, it would immediately result in acute financial problems.

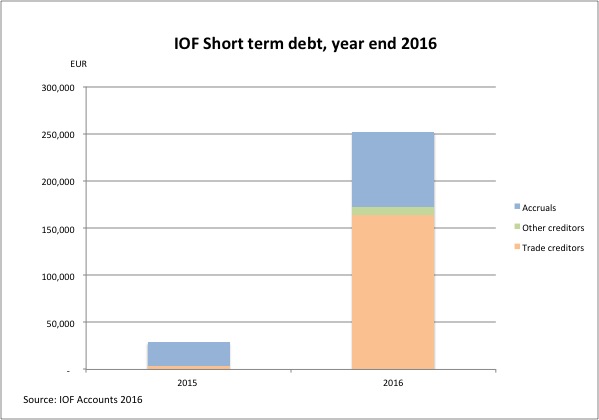

Trade creditors

These are invoices received, accepted, but not yet paid. The year end total jumped from €4000 in 2015 to €164,000 in 2016. Could it happen that bills amounting to 20% of the budget were received only in December? Or did the IOF leadership decided to “stretch” the suppliers (i.e. pay the invoices with a delay), to ensure basic liquidity?

The jump of total short term debt from €29,000 to €252,000 is a worrying sign, especially for an organisation with dwindling reserves.

Other debtors, other creditors

It is unclear what is behind these items. (national insurance could be one guess) In any case, they are small at €9000, and cancel out each other.

Prepayments, accrued income

A surprisingly large item at €52,000 (compare it to only €900 in 2015). This represents either payments made in advance for services not yet consumed; or income earned already in 2016, but not yet billed. A bit of a surprise item…

Accruals, deferred income

Another surprisingly large item almost at €80,000 compared to €25,000 in 2015 (see chart of short term debt). This represents services already consumed, but not yet invoiced (for example, partially completed IT work), or pre-payments received for services yet to be delivered. It also includes €27,000 accrued vacation cost and related social costs.

In essence, this is another €80,000 that improves the bank account temporarily: cash to be paid in 2017, or cash already received in advance with no service delivered yet. But eventually it has to be paid.

Net cash position by the book

The €37,000 represents the net cash position of the IOF at the end of 2016. It represents less than 5% of the annual budget. It shows also a major drop compared to the €100,000 net cash position at the end of 2015.

But some of the accounting items above may not be monetized for various reasons. So when we try to understand the practical cash position of the IOF, we have to make some adjustments.

Inventory

As discussed above, whatever the inventory is (for example brochures), it is unlikely to represent a cash value. Hence, we have to deduct it to estimate available cash reserves.

Brazil debt

This is the remaining €10,000 of the €16,000 Brazilian debt settlement after WMOC 2014. This is a strange item for the fact that it is classified as short term debt in the accounts (i.e. due within 12 months) despite the fact that part of it is not due before end of 2018. Strangely enough, no long term debt is listed at all. Looks like an accounting contradiction on the face of it. It may be considered even as a misleading item.

The key point for our purposes is that this debt cannot be taken as “cash equivalent”. Partly because it is in-kind contribution of development services by Brazil, and partly because it is earmarked for South American regional development specifically devised with the aim of Brazilian debt reduction. The IOF will never see cash of this.

Other debt

Various Council minutes (last time #183, January 2017) discussed outstanding debt of members, some of them past-due from 2014 and 2015. The amount is unclear, but 7 members were threatened with suspension in January. With their membership fees likely to range between €100 to €500 and up to 3 years, an estimate of €5000 was made as debt that may not be available as cash.

Adjusted net cash position

This is the estimated practical net cash position of the IOF at around €16,000, or at around 2% of its annual budget.

This is practically nothing for an organisation the size of the IOF with annual budget between €800,000 and €900,000. A this net reserve corresponds to a single week of average expenses! Any shortfall of the revenues, or even delay in the collection of monies could result in financial issues that may affect the whole sport.

In the next post we’ll discuss further details on how the IOF ended up in this precarious financial situation.