This post is not another one about the ethics of the IOF, but about elections. The title comes from a classic American protest song of the 1960s by Tom Paxton.

Many, many moons ago, in high school, my English teacher used American protest songs to liven up his classes and to make us learn more than just proper grammar. His unorthodox methods eventually earned him even a CBE, but that is another story. These days when I think about the IOF I often recall Tom Paxton’s song about how children are taught to avoid questioning the status quo.

Tom Paxton saw the stability of the US political system a hindrance to progress and accountability. The stability built into the IOF governance system may well be a hindrance to the development and accountability in orienteering.

I learned our government must be strong

It’s always right and never wrong

Our leaders are the finest men

And we elect them again and again

You can find the original here on Youtube.

It seems that the current IOF governance system is a key component of the issues around the federation. The checks and balances that are supposed to ensure that the Council works for the general good in practice do not really work.

These include, but not limited to the following:

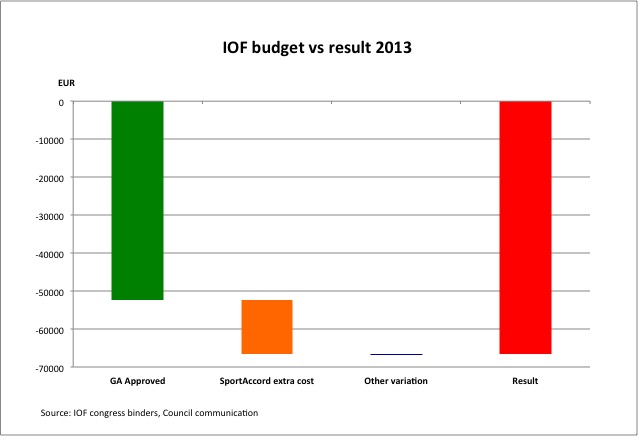

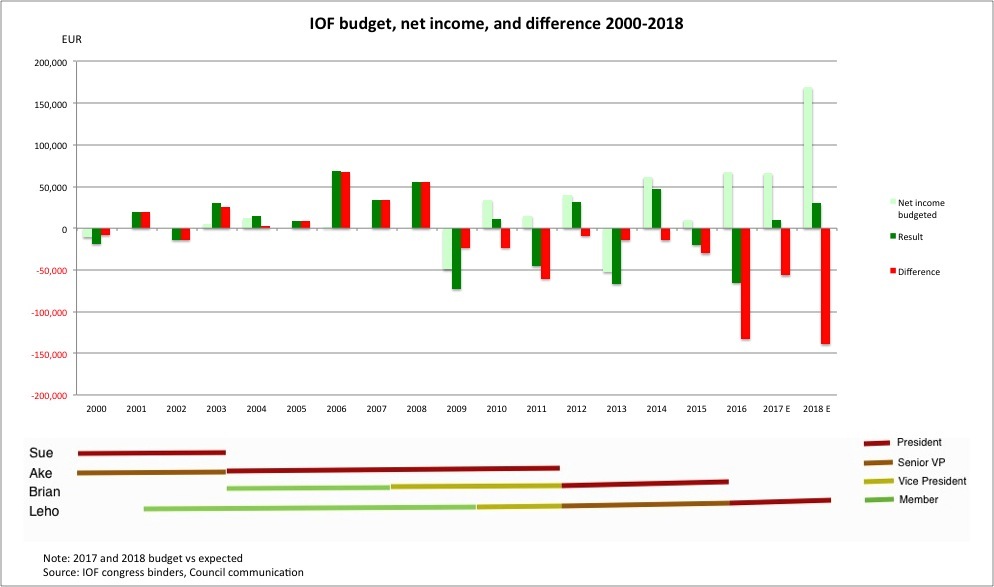

- There is no control over the Council between the General Assemblies (i.e. on 729 days out of 730), thus the President and Council does what they want, including modifying GA decisions at will (the most obvious is the modification of the budget only months after approval – here and here )

- There are no consequences for giving information to the General Assembly that may raise serious questions around its reliability (the 2016 financial status is probably the best documented one here)

- There are no accountability for actions (or in some cases inactions) that could raise serious ethical questions in a more disciplined environment. (see here a few examples)

The contested elections would provide the ultimate checks and balances, but in practice they do not exist. Just the opposite: the IOF election system provides the stability for the Council to stay in place. There is stability derived from the low number of candidates, from the system, and the culture of Council itself.

Stability in the numbers

On paper the General Assembly elects the President and the Council, but in practice they have little choice. A few charts speak better that thousand words:

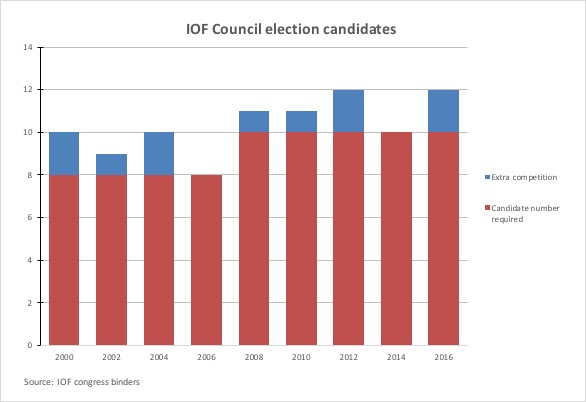

I do not have hard data from previous years, but nobody I spoke to could remember another occasion other than 2012 since 1961 (28 elections altogether) when the election of the president was contested. Sorry to say, but President Putin and President Erdoğan have to face much more competition in their quest to retain their position. It seems that IOF Presidents stay in position unchallenged until they want.

The number of candidates for Council positions is not much higher. In fact, the total choice offered over the last 9 elections is remarkably similar: 10 for 9 for president (11% extra) and 93 for 82 (13% extra to choose from) for Council positions.

(for simplicity I combined the number of candidates for vice president and council member, though they are elected separately)

The number of people actually facing election is far less due to low number of candidates and set quotas (at least 2 of each gender and at least 2 from outside Europe). In 2016 three people were “elected” with no competition. In 2014 the whole Council, all the eleven people, took their position with the General Assembly given the possibility other than to applaud them.

Funnily enough, the Council’s trump card in any discussion when they face arguments from the experts of support and discipline commissions is that they are the “elected body” to make decisions for the sport. Yes, elected for the lack of choice.