Before we start to discuss the vulnerability of the IOF’s financial situation, it is important to clarify some concepts, around financial difficulties. Most of the visitors of this blog (and happy to see already 1300 unique visitors just over the first 10 days of July!) probably know little about the concepts of financial difficulties of organisations. So we have to clarify some basic ones to be able to have meaningful discussion.

Volunteer member based organisations (clubs, federations, etc) typically run very simple cash based finances, often with little or no non-cash assets. The IOF is no exception. The book value of fixed assets was only €10,000 out of the total €145,000 at the end of 2015. The rest was cash or cash-like asset (money expected and money owed within one year).

The only two basic concepts that you need to understand are as follows. I tried to explain them in layman’s terms to avoid the sometimes confusing language of accountancy as much as possible – while risking being excommunicated by finance professionals.

- insolvency: when there is no cash left to pay the bills, or in other words no liquidity left – AND the ones whom you may owe money (e.g. employees, utilities, service providers, bank, tax office, etc – what they call altogether “creditors”) decide to wait no more.

Note: one may be wealthy in general, maybe even own huge property, but if there is no cash left, only angry creditors circling around you, that means insolvency. - technical bankruptcy: when the value of what you own (either what you have in hand or as a firm promise – called “total assets”), is smaller than your obligations (whatever money you owe others in unpaid bills or in cash advance received – called “total liabilities”). It is technical, because you will get into trouble only if everybody you owe something would ask for it. That is rarely the case. Nevertheless, you live on borrowed time. Your net “savings” are less than zero. It is also called “negative equity”.

Note: one may have lot’s cash, but if total assets are less than total liabilities, that means technical bankruptcy. The cash in your pocket belongs to somebody else, just not paid yet.

These concepts are simple, but may be tricky to grasp when written down. So instead of getting into lengthy explanations, I would like to introduce you Orienta, a lady artist in her mid-50s, and explain these concepts showing the problems around her finances.

Meet Orienta

Orienta was an artist with a small, but devoted followership who were rushing around with little painted pictures. She was living mainly on allowing charity festivals to use her name, and she charged them a fee. She also got some money from her fanclub every year, and some little from grants and the odd sponsor. She tried to earn some money on her own, but that wasn’t very successful. You know, artists….

Many dreamt about a happy and enduring relationship with Orienta, but she was capricious with most. She had a sweet spot though for a skinny tall French guy, whom she showered for over a decade with precious bijoux most of us never even dared to dream of. Ah, c’est la vie… But here we want to discuss not Orienta’s romantic life, but her finances….

… and her finances were not in good shape.

At around 2005, in her mid-40s, Orienta got bored of living in a cheap and cheerful way on €20,000 a year. She decided that she should live a high life by her mid-50s, spending close to €100,000 a year. As you can imagine, this has stretched her finances quite a bit. Her main hope was that by showing a more upmarket lifestyle, she could be invited to the largest, most glamorous art festival in the world, organised every four years, where participating artists are given generous support they could live on until the next festival.

Orienta’s finances were cash based. She had no house or car. She only had a computer and a phone worth €1000. She had no debt (who would lend to an artist with no property?), and she did not lend anything to anybody for the simple reason that herself could barely make ends meat.

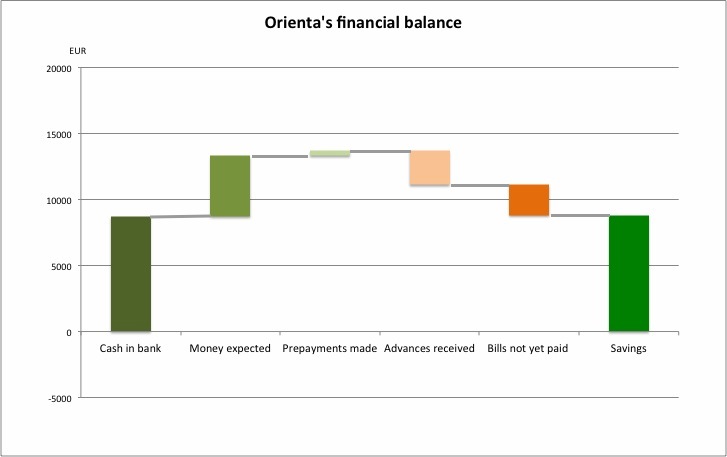

She had €10,000 savings at the end of 2015, so for simplicity we disregard the small value she had in gadgets. Her financial balance, all cash or equivalent, looked like this:

This looks fine for somebody with reliable income and a total of €20,000 or so annual expenses. It may get iffy, if ones expenses are around €80,000, with more or less matching revenues – and it turns out that €30,000 of the revenue may never materialise.

To make matters worse, 2016 was not a good year for Orienta. Her accountant told her that she did not make enough money to cover her expenses. That did not really bother her. She still saw a positive balance on her bank account. She was also getting immune to the warnings of her accountant, who was telling her for the last 8 years that things would not end well.

Considering all that we can have a look at the possible financial problems Orienta may face.

Insolvency

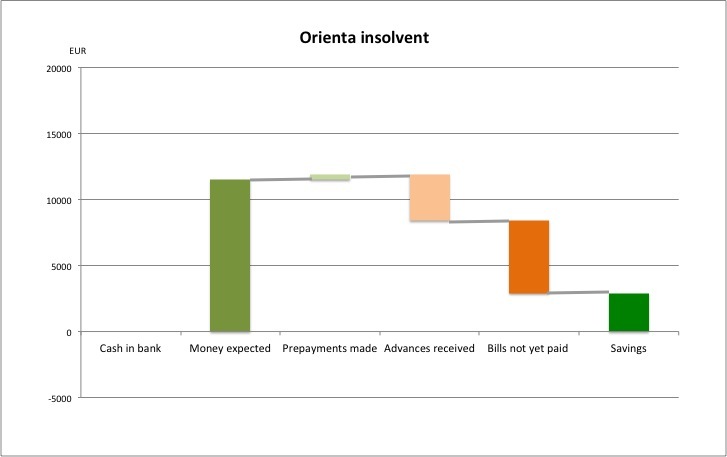

When no cash left to pay the bills. With lower and lower reserves, Orienta may get into trouble, not only if her revenues come below expectations, but also if some of her revenues expected do not arrive in time. A few years ago that was the case with a Senior Citizens Festival organised in the South. It took almost a year instead of a month for the organisers to pay Orienta. In fact, some of the money expected from that festival years ago still has not yet arrived. A repeat situation like that may change Orienta’s financial balance the following way:

As you can see, she still has some savings, but no money left on the bank account. She tried to squeeze out more money from future organisers as advance payment. She also started to delay paying her bills. But there were just too much money that has not arrived yet compared to the reduced savings.

A delay of €12,000 compared to the €4000 outstanding in a typical year would have meant no problem years ago, when she had savings of over €20,000. But with eroded savings she could easily get into insolvency if things work out less than ideal.

Of course insolvency materialises only when creditors (including employees, utilities, service providers – all the ones whose salary/bill was not paid yet) get too agitated. As long as they tolerate not being paid, one can keep the cash and delay the onset of insolvency by paying only the most loud ones, hoping that things turn out for the better.

Technical bankruptcy

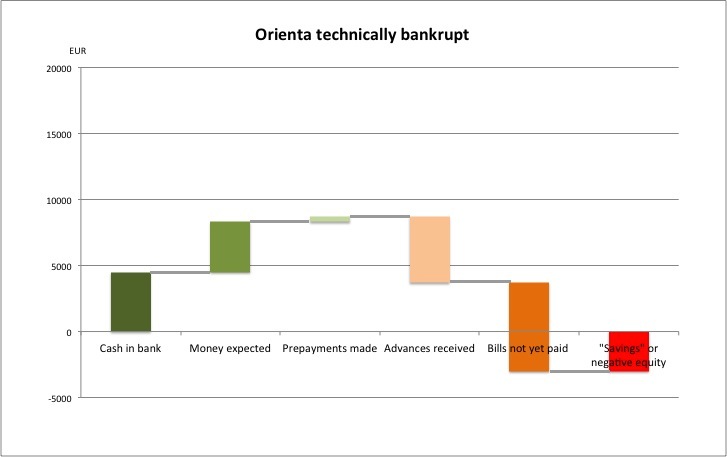

When your obligations exceed the value of what you have, or if you prefer, liabilities exceed assets and you are left with negative equity.

This could happen, if Orienta keeps spending more than her revenues. As you can see in this example, losing all her savings (and more!) does not necessarily mean that she has no money left in the bank. As long as she can delay paying her bills and get prepayments, she could still live as if nothing happened. It is another matter, that with a big chunk of unpaid bills she would get into deeper trouble. This is also a situation when Orienta might start to build up credit card debt – hoping for a brighter future – if anybody would trust her with credit.

The key difference between insolvency and technical bankruptcy is that in the latter case Orienta manages to keep some cash by getting more advance payments and can delay the payment of her bills. But as you can imagine, this is not sustainable for a longer period.

In many developed countries in similar situations directors of organisations (boards, councils, etc) are obliged by law to declare a technical bankruptcy (balance sheet insolvency, if you prefer), for the reason to avoid developing a more difficult situation that would be even more detrimental to employee and other suppliers. Technical bankruptcy may look like a paper exercise for the uninitiated, but it carries a strong signal that the business is not viable in its current form. Unless something changes radically, insolvency is unavoidable because you cannot stretch your creditors indefinitely. Of course, boards and councils tend to be optimistic about the future and often assume that radical change may happen only for the best. That is why in many countries the law requires them to stop trading within a limited period after they lose all their reserves/equity.

***

Orienta is not in financial trouble yet, but with dwindling savings after many many years of spending above her means made her financial position vulnerable. Increasing her expenses fourfold made this vulnerability even bigger. Relatively small negative variation may result in her getting into trouble. Either becoming insolvent, if her payments arrive late and she cannot delay paying her suppliers, or technically bankrupt, if she can delay paying her bills, but in the meantime losing all her savings.

And that famous, most glamorous art festival organised every four year? Could Orienta just keep spending and show a lifestyle that may get her an invitation and loads of money from then on? Difficult to believe. The organisers know that the money they pay is attractive. There is a long queue of other artists wish to participate. A starving artist in financial trouble is unlikely to be a preferred candidate for being invited – unless their presence attracts hundreds of millions of additional viewers. That is not the case for Orienta.