Over the past couple of months there were three apparently contradicting statements made by highly respected bodies of the IOF about the use of Anti-Doping monies in 2018. The audited 2018 Annual Report signed in April 2019 appears to be in contradiction with the Council minutes of January 2019. In return, the statement made by the Ethics Panel in May 2019 appears to be in contradiction with the 2018 Annual Report. The honesty and professionalism of these bodies are unquestionable. The apparent contradictions are part magic, part mystery. The IOF Anti-Doping finances are surrounded by magical mystery.

Apparent contradiction

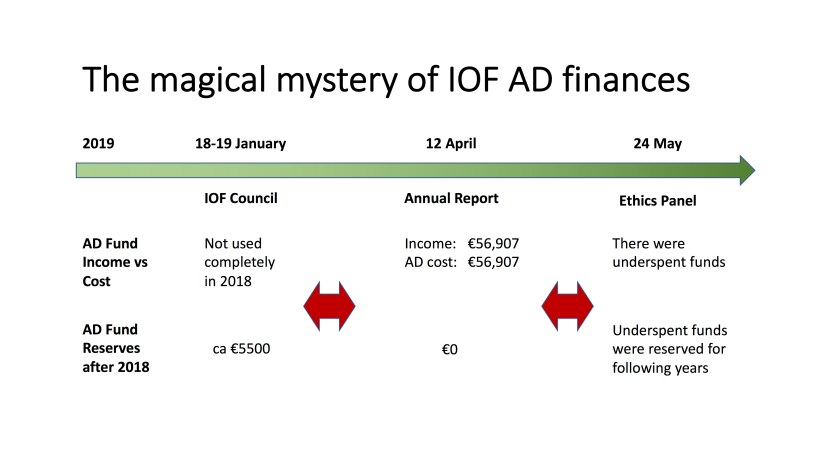

The following chart shows the essence of the apparent contradictions with the details fleshed out below:

January Council meeting

From Council minutes #193 of 18-19 January 2019

Looks like clear information from an unquestionable source:

a reserve of €5500 of underspent AD monies.

The only minor point that one might add is that 2018 is not the second year of the “AD fund”. It has existed already in 2016, but one should not expect all distant details remembered by IOF Office.

The 2018 Annual Report

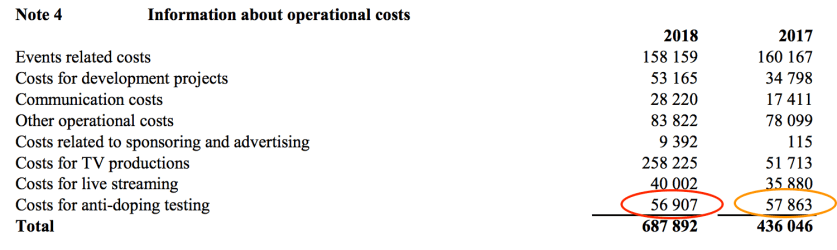

The 2018 Annual Report was signed by the Council on 12 April. It was audited by Ernst and Young who have not found any issues.

Looks like clear information from an unquestionable source:

In 2018 the IOF spent all the money, exactly to the euro, that was collected for Anti-Doping.

So the “AD Fund” is shown to have €0 surplus in 2018, and an overspend of €1000 in 2017. Nothing to be reserved. Not shown here, but you may check the 2016 annual report in the 2018 Congress Binder to see that in 2016 the AD Fund income was stated as €39,941, and AD costs as €40,659. An overspend in 2016 too, and thus no reserves to talk about.

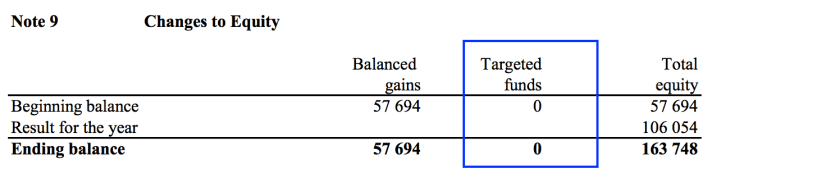

It is not specified in the Annual Report what would be categorised as “Targeted funds” under Swedish accounting standards. We may assume from all the IOF communication that the “AD Fund” is a targeted fund, even if a true targeted fund is likely to be detailed within the accounts. The AD Fund is not detailed separately within the IOF accounts.

In any case, no signs of any €5500 reserve, neither here, nor in any other place in the Annual Report. It is a mystery.

Interesting to note that according to the Annual Report the AD costs in 2018 matched the AD Fund income to the euro. This coincidence of income and expense looks like magic, especially considering that according to the Council minutes there was “unfortunate cancelling of some testing at the end of 2018” and a reserve of ca €5500 was created.

The Ethics Panel statement

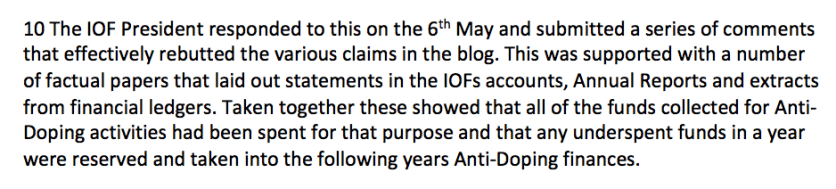

In their letter dated 24 May the Ethics Panel wrote the following under Section 10:

Looks like clear information from an unquestionable source:

there were monies reserved due to underspent funds, and they were taken into following years Anti-Doping finances.

You may read the whole letter in my previous post about the Ethics Panel investigation based on an IOF report against this blog.

Unquestionable sources

Needless to say, but never hurts to repeat, that this blog keeps all IOF officials and activists in the highest respect they deserve. The integrity and the professional standards of the above sources are unquestionable.

The IOF Council would immediately step up if they would see anything less than appropriate. There should be no doubt about that. Long gone the days of 2013 when the IOF Council sat quietly when they were informed that the then President presented alternative facts about a member federation. Now, equipped with the moral compass of the IOF Code of Ethics, there is no question that the Council would step up and correct immediately all misstated information they may come across.

Ernst and Young, the auditors of the IOF, is one of the largest and most respected professional services firms in the world. Its wikipedia article lists only around two dozen recent accounting and auditing scandals to its name; a rather good performance in its class. One may note that EY, as the auditor of Danske Bank, was reported in April 2019 to the Danish police by Danish authorities for its role in the money laundering case labelled as Estonian Laundromat by Bloomberg. But unfortunate events in distant countries should not carry any implication on the professional standards of EY Sweden.

The Ethics Panel is the Ethics Panel IOF. By definition it is the most ethical, and thus the most unquestionable of all IOF bodies.

Possible solutions

Facing this magical mystery of IOF Anti-Doping finances I talked to some accountants familiar with international finances. Without getting into details of their experiences, let’s say that if there is an accounting trick that they did not see, that probably does not exist.

They came up with a couple of ideas detailed below that might explain the magical mystery of IOF AD finances. It has to be declared here and now that this blog does not support any of their ideas. The ideas of season financial professionals do not assume full integrity of everybody involved in IOF activities. This might be seen as disrespectful to IOF officials, and this blog cannot possibly support that position.

Creative accounting

One idea mentioned was the introduction of a “balancing item” to the 2018 AD costs. The magical coincidence of AD income and costs could suggest that something similar happened. Accounting for reserves is a pain in the neck, better to be avoided. Allocating an appropriate part of the salary of the AD officer, part of office cost, or even part of the salary of the CEO to AD costs is easy, especially when no in-depth details of the “AD fund” are public. The apparent contradiction between the Ethics Panel statement and the Annual Report was explained with lack of communication around such technical details between the accounting department and top management.

This might sound plausible in some less respectable organisations, but this blog should reject this idea in relation to the IOF. It would imply a level of gaming with accounting figures that must be excluded as an option when it comes to the highly respected operations of the IOF.

Double set of books

An interesting, but nevertheless unacceptable idea was the use of double sets of books (at least for some activities) within the IOF. One for budgetary purposes, the other for practical spending. The apparent contradictions above could be explained by the mixup of the two books: management is aware of the reserves, while for accounting purposes no surplus is shown. The apparent contradiction was suggested to be the result of mixing up references to the two sets of books.

Needless to say, this idea something this blog should not entertain in any way. It is just shown to illustrate what some less respectable organisations known to be doing.

A simple mess

An interesting idea mentioned was that the finances of the IOF could be in a bit of a mess. This could explain any level of contradiction observed. This might be also an appealing explanation for some for its simplicity. It is a basic scientific principle that a simple theory that explains an observation is considered to be more credible than a complicated explanation.

It must be self evident that this blog refuses to grant any credibility to this idea. It might be true that the IOF leadership could not replicate its approved budget in 2017, or that it provided inconsistent and contradictory information on IOF Anti-Doping tests. But any suggestion that would imply that things are not in top notch order within the IOF could be seen again as disrespectful to the IOF leadership, and thus it should be rejected by this blog.

* * *

The magical mystery of IOF Anti-Doping finances remains to be explained. The possible solutions mentioned above were ideas of accounting professionals based on published numbers and statements. I have also asked guidance from the CEO of the IOF and the Ethics Panel on how to resolve the apparent contradictions between their statements and the Annual Report. I will keep the readership of this blog updated with their replies. If you have any suggestions, please let me know via the Contact page of this blog.