I just wanted to provide an update on the mystery of the IOF AD finances based on the information received from the CEO of the IOF that I very much appreciate. This brings us closer to understanding the numbers around the special AD tax levied on athletes and organisers, but it raises quite a few additional questions about the transparency of IOF financials.

According to our correspondence,

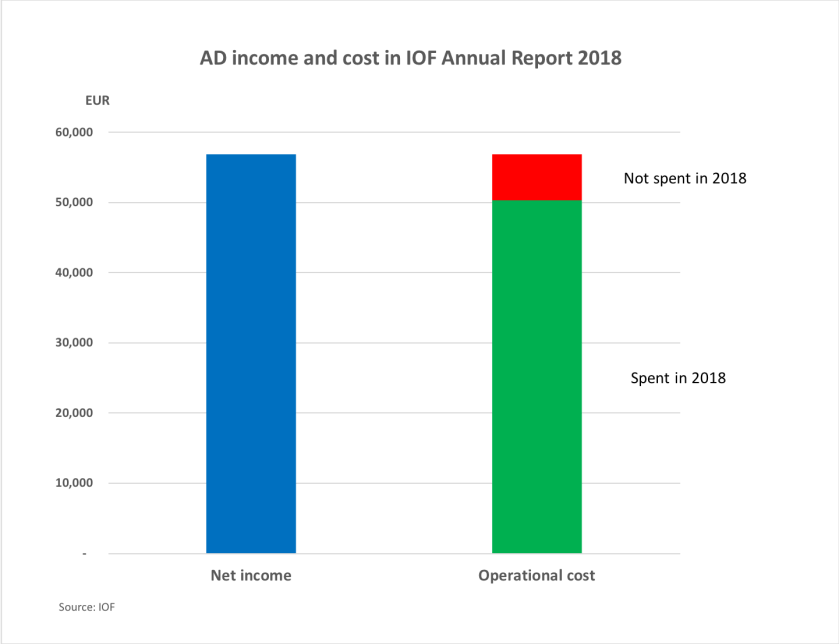

“The amount collected is 584 736 SEK and that is exactly what is shown in the Annual Report. 517 433 SEK was used for testing during the year and, as stated below, 67 303 SEK is reserved as pre-paid income to be used in 2019.”

“At year end (2018-12-31) the amount of SEK 67 302,81 was reserved on the balance sheet in account 2900 Accrued costs/pre-paid income, and in doing so the corresponding transaction was made in the anti-doping fund account thereby making income and cost for the year equal.

On 2019-05-01 this pre-paid income was released back to the anti-doping fund account for use in testing to be conducted during 2019.

The above was agreed and approved with the IOF Auditors as the correct way of reserving the money for future use.”

This is illustrated below in euros to correspond with the numbers shown from the 2018 Annual Report in the previous post. This explains why the 2018 AD revenue and cost was set equal at the level of €56,907, although only €50,357 was spent in 2018. There should be also a €6,550 item buried within the €109,213 liabilities to compensate for it. Sadly, no details on this €109,213 liability item is available within the IOF Annual Report.

This is an unusual approach. Without getting deep into accounting, stating a €6,550 cost item in the 2018 accounts that had nothing to do with 2018 (as cost) would be a big no-no in the dozen or so financial regulatory systems my accounting friends and me are familiar with. Accounting for the AD Fund separately as a targeted fund, or declaring a lower income by €6,550 for 2018 (and reserving the rest as pre-paid for 2019) would have been a more standard approach. Sadly, I could not get info from Swedish friends just now, but this is less relevant, as this blog is not about discussing accounting nuances.

There are two interesting points that may be of interest to the readers of this blog:

First, the IOF Annual Reports seem to be very relaxed when it comes to the timing of some line items. Financial professionals with investigative minds would immediately ask if there are any other items on the profit and loss statement of the IOF that contain elements related to other years.

Second, the above confirms that based on the IOF Annual Report orienteering folks cannot understand how the IOF spends this special €60,000 or so Anti-Doping tax collected from athletes and organisers. As a reminder, not only the €30 collected for each “Athletes Licence” goes into this fund, but organisers of major events should also “donate” €500 to €1150 per day. Details of that were shown in my earlier post that raised questions about the IOF’s AD activity (and was immediately reported to the Ethics Panel by the IOF leadership).

In addition, there is no 2018 Anti Doping report published (as of 6 August 2019), no details published on the use of the special “AD Fund”, and apparently no questions were asked by member Federations sticking to the good old “just pay without questions” attitude.

Athletes and organisers may have to remain satisfied for the time being by just paying whatever the IOF leadership decides in the name of a good cause.